The Receipt Problem in Tax Payments: 'Client Paid' Isn't the Same as 'We Can Prove It'

Tax services firms can initiate payments. They cannot easily prove what was paid, when, or who authorized it once a notice arrives months later. EO 14247 takes the 2026 filing season fully electronic, and the proof workflow is still a shared drive.

By Solon Angel

Something I have heard four different ways in the last month, from four different firms, in four different parts of the country. The client paid. We just cannot easily prove what they paid, when, or who authorized it once a notice lands six months later.

That is the quiet sentence behind almost every tax payment conversation right now. Nobody wants to say it on a sales call. The admin team knows. The partner who signs the engagement letter knows. The insurance underwriter who renewed your policy this year definitely knows. Tax services already account for roughly two thirds of professional liability claims against CPA firms. Filing errors have overtaken bad advice as the leading cause. The trail behind a payment is now where the risk lives.

Here is what the operational reality looks like in 2026. A regional firm described their proof workflow as admins collecting payment confirmations, scanning them, dropping them into a shared drive, and trusting human memory for the rest. A boutique firm working with high net worth clients walked me through the moment a seven figure quarterly estimate lands in a client's account three months after approval. The client freaks out. The firm has to reconstruct, from email threads and screenshots, that the authorization actually happened. The same firm flagged a case where one payment was made twice. A mid sized firm in the midwest told me their current process is 'terrible' and that one of their clients missed a deadline because they could not get a state portal account set up in time. A national tax services firm did not ask whether payments could be initiated. They asked what proof would actually survive an IRS controversy case, citing prior fights where the taxpayer's bank had a record of payment and the IRS said it had not received one.

Different firms. Different segments. Same sentence underneath. We can pay. We cannot yet defend the payment.

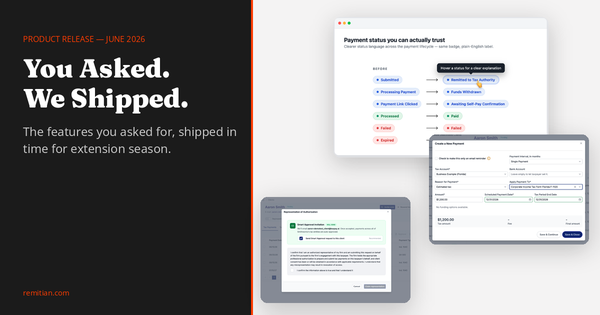

The reason this is suddenly urgent is Executive Order 14247. Starting with the 2026 filing season, third parties transacting with the IRS on behalf of clients are expected to move to electronic payment methods, and additional transaction types are being rolled out that require updated third party systems. To stay in Circular 230 compliance, practitioners are being pushed toward EFTPS or Electronic Funds Withdrawal, which raises the bar on documented authorization and routing accuracy in a way the old paper world simply did not. The procedural guidance going around right now tells tax pros to verify client banking data before filing and warn clients they have 'only one opportunity' to enter the data correctly. That is not a software vendor marketing line. That is the official posture.

Read that sentence again. One opportunity. In an all electronic regime, the audit trail is the deliverable. Not the payment. The proof.

This is the part most firms have not internalized yet. When payments moved off paper, the failure mode changed. It used to be a lost check. Now it is a missing screenshot. A confirmation email in someone's inbox who has since left the firm. A spreadsheet column that nobody updated for the second quarter. The payment itself is the easy part. The story you can tell about the payment, in twelve months, in front of a client who is angry, or in front of the IRS, is the hard part. And almost every firm I talk to is running that defense on a shared drive.

I am not writing this to sell anything in particular. I am writing it because the same observation keeps showing up on calls and it is starting to feel like the industry is one or two bad cases away from realizing the proof side of tax payments needs the same modernization the payment side already got. We spent a decade fixing how money moves. We did not fix the receipt.

That is what I keep thinking about this week.

Solon Angel is the Co-Founder and CEO of Remitian, the tax payment infrastructure platform for accounting firms, banks, and their clients.